New research by the IGF and the Organisation for Economic Co-operation and Development (OECD) has found that many resource-rich developing countries use tax incentives in the hope of attracting mining investment. Roughly two thirds of the countries surveyed give corporate income tax concessions to mining investors either in the law or in mining contracts, or, in many cases, in both. Slightly less than half grant a complete tax-free period (“tax holiday”), wiping out the entire tax base for between three and 12 years.

A tax incentive is a favourable deviation from the general tax treatment that applies to all taxpayers. As an example, while the statutory tax rate in Sierra Leone is 30 per cent, the government has given two iron ore mines a lower rate of 20 per cent, thereby forgoing USD 131 million in revenue between 2014 and 2016. While incentives may sometimes be necessary, the Business and Industry Advisory Committee warns that even mining investors will “discount regimes and incentives that are ‘too good to be true.’”

Supplementing wider work undertaken by the Platform for Collaboration on Tax on tax incentives, the IGF and OECD have published Tax Incentives in Mining: Minimizing Risks to Revenue, the first guidance document devoted to tax incentives in mining specifically. The practice note focuses on the ways that mining investors may change their behaviour in response to tax incentives to maximize the tax benefit beyond what government intended—the tax base erosion and profit shifting risks.

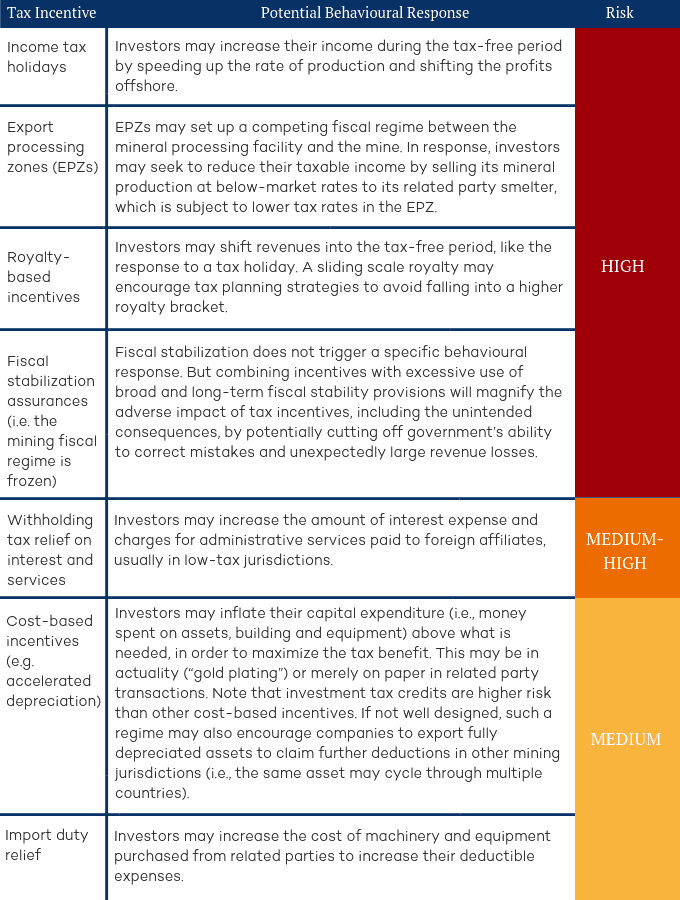

For a list of the ways in which investors may exploit mining tax incentives, see the table below.

A common way for host governments to lose out on mining revenues is through excessive interest deductions. Companies can finance a mine through debt or equity. Debt is treated differently to equity for tax purposes: interest payments on the debt can be deducted from taxable income. Consequently, companies have an incentive to increase their debt levels, in particular for mines in high-tax countries.

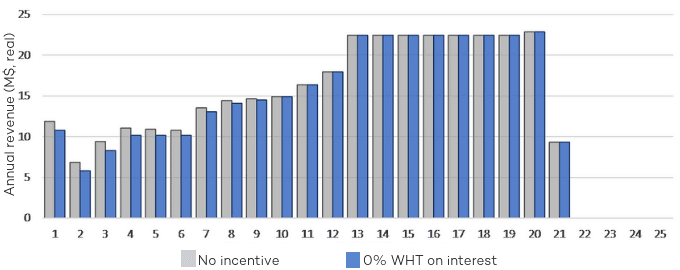

In general, governments impose tax on interest payments (referred to as withholding tax). If they offer a lower rate, it follows that they collect less tax. This scenario is shown in Figure 1, where the rate of tax is reduced from 15 per cent to zero. The figure was produced by the IGF Financial Model, an open source financial model that can be used by governments to estimate the cost of tax incentives. Under this scenario the government forgoes $6.4 million in revenue.

NB: the grey bars represent the revenue that government would have collected without the incentive, and the blue bars represent the revenue collected after the incentive.

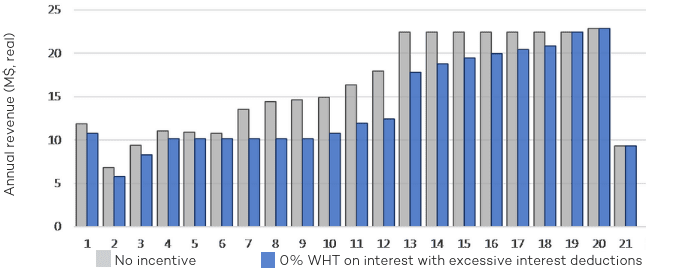

By lowering the rate, the government provides an added incentive for a company to load up the mine with debt, as well as charge above-market interest rates to reduce local taxes and shift profits overseas. Under this scenario, the government loses a further $42.6 million in revenue.

Before agreeing to any tax incentives, governments should use a financial model to estimate the cost of incentives and their impacts on investment decisions. Unfortunately for Cote d’Ivoire, it was only after the government had granted a five-year tax holiday to Yaoure gold mine that it developed a model with OpenOil to examine the impact of the incentive. In doing so it learned it had given away USD 129 million despite the mine having a healthy rate of return without the concession.

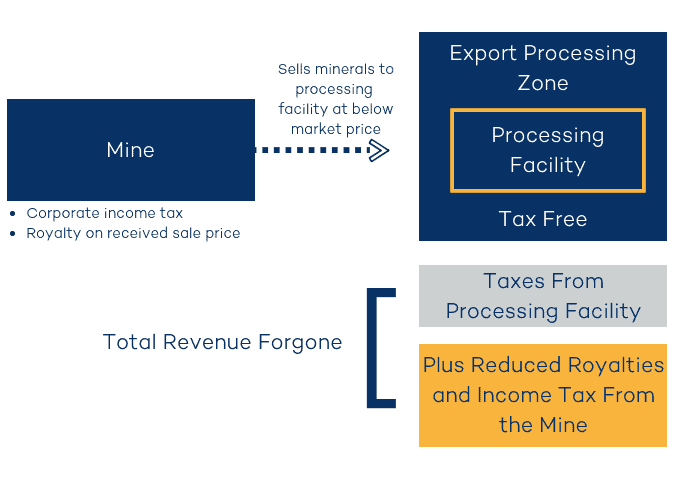

Another way that governments may lose mining revenues is through underpricing of mineral sales. As an example, if a related party smelter is set up in an export processing zone (EPZ) that offers partial or reduced tax rates, there is an incentive for the mine, which is subject to normal tax rates, to deliberately underprice its minerals to reduce its taxable income and shift profits to the smelter in the EPZ.

Figure 2. Mineral sales to export processing zone

Governments control the design and use of tax incentives to attract mining investment. If incentives are overly generous or poorly drafted, governments should not be surprised to find that investors have maximized the tax benefit in ways they did not anticipate.

Tax Incentives in Mining: Minimizing Risks to Revenue can help governments think through the design and use of incentives so that they avoid unnecessarily giving away valuable revenues from the exploitation of their finite, non-renewable resources.

The practice note is supplemented by an open source beta-stage financial model for estimating the revenue foregone from tax incentives in mining. There is also a supplementary guidance document to the model, which is accessible online.

Table 1. Type of tax incentive and the related behavioural response